This newsletter is really a public policy thought-letter. While excellent newsletters on specific themes within public policy already exist, this thought-letter is about frameworks, mental models, and key ideas that will hopefully help you think about any public policy problem in imaginative ways. It seeks to answer just one question: how do I think about a particular public policy problem/solution?

PS: If you enjoy listening instead of reading, we have this edition available as an audio narration on all podcasting platforms courtesy the good folks at Ad-Auris. If you have any feedback, please send it to us.

Global Policy Watch #1: Deadly Advice

Bringing an Indian perspective to burning global issues

- RSJ

There are consultants and investment bankers who floor you with their presentations. And then there is Mckinsey & Co. When the ‘smartest guys in the room’ speak, you watch them transfixed. To use Coleridge’s immortal words:

“He holds him with his glittering eye—

The Wedding-Guest stood still,

And listens like a three years' child:

The Mariner hath his will.”

You are often the wedding-guest and you listen to them like a three-year-old.

I guess it didn’t exactly work out that way over the past few months when Mckinsey was answering questions about its role in abetting the opioid crisis.

Not Caring About the Consequences

On Feb. 4, McKinsey & Co., the management consulting firm, announced a $573 million settlement with 49 State Attorneys General for its past work for opioid manufacturers. In Nov. 2020, Purdue Pharma pleaded guilty to criminal charges of not doing enough to combat the opioid epidemic that has ravaged the American heartland largely on the back of aggressive marketing of its flagship product, OxyContin.

Purdue acknowledged it looked the other way when the prescription drug was diverted to the black market, it misled regulators to boost its manufacturing quotas and it paid doctors for random speaking gigs that were a way to reward them for writing more prescriptions for OxyContin. The costs to society were dramatic - over two million addicts and about half a million opioid-related deaths in the past two decades. There’s no other way to put it; Purdue Pharma was an evil enterprise that deliberately sold products that killed people while profiting enormously from it.

And Mckinsey advised Purdue from 2004-19 on how to do this well.

On Feb. 4, Kevin Sneader, global managing partner of Mckinsey, wrote a memo to all his colleagues on the settlement. It contained the oldest excuse in the book - we weren’t doing anything unlawful. That’s consulting-speak admitting we were unethical:

“Indeed, while our past work with opioid manufacturers was lawful and never intended to do harm, we have always held ourselves to a higher bar. We fell short of that bar. We did not adequately acknowledge the epidemic unfolding in our communities or the terrible impact of opioid misuse and addiction, and for that I am deeply sorry.”

And it contained this gem:

“It is also a key reason why we chose the course of action announced today since it allows funds to be deployed quickly and directly to victims of the opioid crisis while avoiding a long and protracted legal process.”

I’m not sure there is a consulting equivalent to that old Hindi proverb - “nau sau choohe maar, billi chali haj karne”.

But Mckinsey could use it next time.

The saga has followed a predictable course since. On Feb 24, the 650 global partners of Mckinsey voted to replace Kevin Sneader as its global managing partner. As far as Mckinsey goes, I guess, they have done all they could to put this behind them.

The Slippery Slope In Business

What makes a pharma company that set up its business to save lives go down the path of taking lives? Greed?

There’s always the usual punching bag brought up when something like this happens - the Friedman doctrine. The purpose of a business and its sole social responsibility are to maximise shareholders value. That, according to its critics, gives businesses a free run to do anything. It makes greed legitimate. But does it? We put up a passionate defence of the Friedman doctrine on the 50th anniversary of that paper in edition #70. Friedman, as we have argued before, wasn’t making a case of untrammelled capitalism. In fact, he makes following the rules of the game fundamental to how a business must operate. As he concludes in that paper:

But the doctrine of “social responsibility” taken seriously would extend the scope of the political mechanism to every human activity. It does not differ in philosophy from the most explicitly collectivist doctrine. It differs only by professing to believe that collectivist ends can be attained without collectivist means. That is why, in my book “Capitalism and Freedom,” I have called it a “fundamentally subversive doctrine” in a free society, and have said that in such a society, “there is one and only one social responsibility of business—to use its resources and engage in activities designed to increase its profits so long as it stays within the rules of the game, which is to say, engages in open and free competition without deception or fraud.” (emphasis ours)

Business ethics is often half-jokingly cited as an example of an oxymoron. There are challenges inherent in the market system for a business to be virtuous or ethical on its own. There’s the principal-agent problem, to begin with. The people running the business often aren’t the owners of the business. They have an incentive to maximise their short-term gains at the expense of all others. Then there’s information asymmetry between the business and its consumers. It is not possible for consumers to know everything about the products of a company. They trust the company to make products that are good for them. The company then has the incentive to be economical with the truth. There’s also the collateral damage problem on the society or environment that a business often inflicts. Pollution, for instance. It is what the economists call a ‘negative externality’. How does a business pay for it?

If markets were to be left free from any intervention, businesses will exploit these failures for their benefits. They might make inferior or harmful products, take short-term decisions that hurt their consumers, workers or shareholders, pollute their environment or harm society. You could say in the long-run the markets will figure this out and punish them appropriately. But the social costs incurred by then will be too high.

The Case for Regulations

This is where regulators come in. The only reason for the state to intervene in markets through laws and regulations is to address these market failures. But it is a cat-and-mouse game between the regulators and those who are regulated. Most companies follow the regulations and get on with their lives. Not all. There’s always a temptation to go around them. And it isn’t too difficult. If a company decides to hide or obfuscate the truth, it can hoodwink a regulator for long. We have seen this play out many times over across sectors.

But the case of Purdue Pharma is somewhat unique. It ran its racket of selling OxyContin as an opioid to addicts in plain daylight. Everyone who dealt with Purdue knew of it - patients, doctors, pharmacies, hospitals, auditors and consultants. The competitors knew of it. As did many reporters and writers who covered the opioid crisis over the past two decades in print and literature. Everyone except the regulator, which strictly followed the guidelines and only went by Purdue’s responses to their queries. So long as the responses and supporting evidence that went along with them were fine, the regulators considered their job done. And how did Purdue manage to do this?

Well, there’s Mckinsey & Co.

There’s no other way to put this. Purdue Pharma framed their problem this way - how to maximise the sales of OxyContin that included its abuse by addicts while keeping the regulators away with their smooth but inaccurate responses?

And Mckinsey, the smoothest of the mariner, hath their will (as Coleridge would say) with their presentations. Presentations that did some unique cost-benefit analysis ever in the history of consulting. Valuing human life. Presentations that suggested if Purdue paid $14,810 per “event”, and if 2,484 customers of the CVS pharmacy chain overdosed or became addicted in 2019, Purdue would pay CVS $36.8m that year. There’s more there in those presentations that will shake your faith in humanity.

As other cases and class action suits pile up, it is almost certain Purdue Pharma will cease to exist in its current form. The ‘philanthropic’ Sackler family that owns it will also have its day of reckoning. But what about Mckinsey? A $600 million fine and a change of its managing partner? That’s it? Seems like a fairly low cost to pay for some deadly advice.

The financial sector regulators have learnt from the many financial crises on how to regulate investment banking and advisory businesses. These included personal criminal liabilities, fines and clawback of bonuses paid if a wrongdoing is proven in future. There’s something to learn from them to ensure those in the business of advising corporates bear moral responsibility for their services. Not doing anything unlawful isn’t enough. Else, it is only a matter of time before another partner will be putting up similar slides to turbocharge another unethical business.

But can regulations ever be enough? Like we have seen over and over again, it won’t ever be watertight. Maybe a start needs to be made at business schools - the source of talent for these companies. Tom Peters, the bestselling author of many books on strategy and a Mckinsey alum, writing for FT makes this point:

In my opinion, this is not unrelated to the OxyContin affair. I have long argued that we should “shut down every damn business school”. This rant is hyperbolic, but my reasoning is that business schools typically emphasise marketing, finance, and quantitative rules. The “people stuff” and “culture stuff” gets short shrift in virtually all cases.

I agree. I’m not sure if there is equal importance given to the discipline of ethics as it is given to a course on Options and Futures in any MBA programme. You could structure a beautiful futures contract or devise a compelling strategy for enhancing sales force productivity using what you learnt in a business school. Those models could be terrible for society and your clients could be guilty of using human beings as means and not as an end in themselves. You could plead ignorance about these ideas. Or you could have read Aristotle and Kant at school and asked those questions before you began building your model.

Reading Friedman isn’t a problem. Reading only Friedman is.

A Framework a Week: The Domar Rule for Public Debt Sustainability

Tools for thinking public policy

— Pranay Kotasthane

This newsletter unabashedly bats for policies aimed at accelerating India’s GDP growth. We’ve reasoned out our position in myriad ways in previous editions. And yet, we realise that the sceptics aren’t fully convinced. The ideological challenges to GDP growth first — inequality, inclusive growth, and sustainability — continue to gain strength.

So let’s try another line of reasoning: even if you are in favour of big governments, you cannot escape the prior need for higher GDP growth. Here’s how.

Big governments need more money by way of higher taxation or higher borrowing. In the current economic situation when there are no profits to tax, governments across the world are competing to borrow money for restarting their pandemic-hit economies. In some economies like the UK, public debt has hit its highest level since 1945. Consequently, the interest rates these governments are promising their borrowers (bond yields) are rising.

This higher borrowing comes at the expense of the savings of future generations who will end up paying taxes in repayment of this mountain of debt. Is there a limit beyond which the fetish for big borrowing becomes unsustainable? A classic 1944 paper titled “Burden of Debt” and National Income by Evsey Domar gives an answer.

As the second world war was winding down, governments then faced a situation not different from today — the economic reconstruction needed massive borrowing. The policy orthodoxy at the time opposed wanton borrowing — today’s deficits would lead to tomorrow’s higher tax rates, they said.

Domar disagreed. Instead, he said that governments running deficits weren’t all that bad especially in times of crises when private investment would decline. Instead, the crucial variable one should be tracking was the national income. With a set of assumptions, he derived that as long as the national income grows at a rate faster than the interest rate, tax rates settle to manageable levels.

While it is true that higher deficits mean higher tax collections from subsequent generations, it doesn’t necessarily imply an increase in the rate of taxation. Provided that the economy grows at a robust rate, a smaller percentage of it hived away as tax can raise the same tax amount as would a higher tax rate raise on a slow-track economy. This is intuitive. For instance, a 12 per cent tax rate on an economy that is stuck at 100 units generates the same tax amount as a 10 per cent tax rate on a faster economy that has galloped to 120 units in the same period. In other words, compound growth counters compound interest.

Domar’s conclusion is simple but profound: the problem of debt burden is a problem of expanding national income.

The chart below illustrates this finding. At constant incomes (stagnant GDP), tax rates keep rising linearly. At the other extreme, when income rises at the same rate as the interest rate (2 per cent in this case), the tax rate remains constant. More interestingly, the sawtooth pattern below shows that even if there were recurrent wars every thirty years requiring recurrent massive government borrowing, tax rates would still be under control so long as the national income keeps growing handsomely.

So, higher levels of public debt are not all bad. The key is to understand how that additional borrowing is being utilised. If this money is invested in a way that accelerates economic growth, debt will be sustainable in the long run. In other words, spending on physical and human capital is desirable, spending on wasteful subsidies is not.

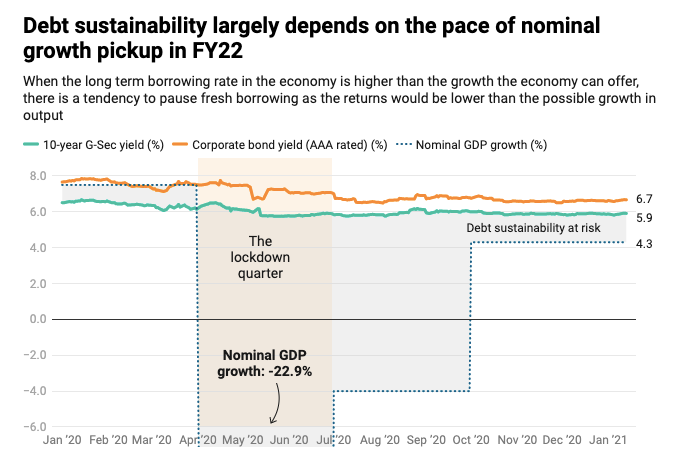

Now, armed with this framework, observe where India is. The interest rate on the government’s 10-year bonds is hovering at the 6.2 per cent mark while the GDP growth has barely turned positive last quarter after two consecutive quarters of negative GDP growth. Even before the pandemic hit, the situation wasn’t all hunky-dory. The slowdown of the last decade means that public debt sustainability has been worsening for almost a decade now.

A chart in Business Standard has a good illustration of this risk. Without returning to higher GDP growth rates soon, even government borrowing will become unsustainable. And if the government doesn’t have the spending power, all other worthy projects of tackling climate change and inequality have no chance of success.

Global Policy Watch #2: The Great Chip Squeeze

Bringing an Indian perspective to burning global issues

— Pranay Kotasthane

If you’re planning to buy a new car, don’t. Because you’re staring at indeterminate delays as the semiconductor IC chips that make your car infotainment and control systems work are just not available in the global market. No one’s quite sure when this shortage would be resolved. Some estimates suggest that nearly 1 million fewer vehicles will be produced the world over in the first quarter of 2021 because of the semiconductor shortage.

This peculiar market condition has been in the news for many weeks now. Two reasons are commonly cited. One, a massive advance purchase order from Huawei in anticipation of US sanctions last year gobbled up available manufacturing capacity. And two, as the demand for vehicles dropped during the lockdown period, contract semiconductor manufacturers shifted focus to meet the higher demand from a much more lucrative segment — phones, data centres, and routers. When the automobile demand eventually bounced back, the manufacturers had no spare capacity to offer them.

While these two are indeed the proximate reasons for the current shortage, the more fundamental cause is a uniquely bottlenecked semiconductor supply chain.

In the 1980s, the semiconductor industry was transformed by the arrival of companies specialising in manufacturing chips on contract. These companies in turn created a new generation of fabless semiconductor design companies which were unencumbered by the huge setup costs (setting up a manufacturing plant needs an investment in excess of $10 billion).

While thousands of fabless companies mushroomed around the globe, the contract manufacturing market kept consolidating with the end result that just one company, Taiwan-based TSMC, does nearly 50 per cent of the world’s contract chipmaking.

Not that anyone was complaining. This extreme form of comparative advantage-led diversification worked perfectly well. The labyrinthine supply chain worked so well in fact that TSMC was hardly known outside the tech world.

And then, the pandemic happened.

COVID-19 exposed the underlying fragility of this supply chain. The overdependence on a handful of contract chip manufacturers became a bottleneck and the supply chain unravelled. In most other markets, higher demand would have been met by new suppliers motivated by higher prices. But even this shock absorption is not possible the case of semiconductors. Setting up a new manufacturing plant costs three-four years, a lot of money, and top-notch talent.

The big takeaway from the current shortage is that the semiconductor industry is being seen in strategic terms. The US plans to get both Samsung and TSMC to set up new plants there while the CHIPS for America Act plans to pump in massive investment for local players. The Indian government too has floated an expression of interest to gauge interest for a semiconductor fab in the country. Europe for its part is also putting in place a plan to help its home-grown players. All this even as China has been pumping in billions of dollars since 2013 for its own version of semiconductor aatmanirbharta.

The moment is right for countries or industry bodies to form consortiums for financing the huge upfront costs of semiconductor manufacturing facilities. I have previously written why semiconductors should be the focus of technology cooperation in the Quad framework.

The lack of redundancy in the current supply chain coupled with the imperative to make supply chains of critical technologies China-free means that the semiconductor landscape is set to change this decade. Expect many policy flip-flops along the way.

HomeWork

Reading and listening recommendations on public policy matters

[Paper] Political Economy of Government Finance in India by Govinda Rao gives a comprehensive overview of important features of India’s public finance story.

[Article] How Covid-19 changes the geopolitics of semiconductor supply chains.

[Article] Rathin Roy discusses why the quality of public debt is just as important as the quantity.

[Article] The Economist asks - Should governments in emerging economies worry about their debt?

Share this post