#28 The State Proposes, and the State Disposes

Price Caps, Franklin Templeton Saga, Guns vs Butter Debate, Naya Daur, and more

This newsletter is really a weekly public policy thought-letter. While excellent newsletters on specific themes within public policy already exist, this thought-letter is about frameworks, mental models, and key ideas that will hopefully help you think about any public policy problem in imaginative ways. It seeks to answer just one question: how do I think about a particular public policy problem/solution?

PolicyWTF: Price Caps, SF Style

This section looks at egregious public policies. Policies that make you go: WTF, Did that really happen?

— Pranay Kotasthane

With governments in the driving seat in these times of crisis, there’s no shortage of PolicyWTFs.

If you thought that price caps were a favourite instrument of the Indian government alone, turn your attention to the city of San Fransisco. The City Hall announced a temporary limit on the commission that third-party food delivery companies can charge restaurants during the COVID-19 pandemic. The logic behind this move in the words of the Mayor:

Restaurants across San Francisco are struggling to stay open. In these tough financial circumstances, every dollar counts and can make the difference between a restaurant staying open, or shuttering. It can make the difference between staying afloat or needing to lay-off staff.

Remember, restaurants there are only allowed to offer take-out and delivery which means third-party food delivery companies such as UberEats are critical for restaurants to operate. Unsurprisingly, UberEats stopped deliveries in some areas of the city on the grounds that this government order limits their ability to cover operational costs.

But that’s not where this ends. The area they have stopped services to is apparently a low-income neighbourhood. So the familiar narrative — ‘rich-companies-discriminating-against-the-poor-in-times-of-crisis’ — has taken hold.

The retaliation by UberEats aside, a price cap on food deliveries is not going to save restaurants. Such moves disincentivise all food delivery companies from adding more staff. Moves to reassure customers that take-out food is safe might work better.

A Framework a Week: Guns & Butter

Tools for thinking public policy

— Pranay Kotasthane

This week I’m rereading Paul Kennedy’s classic The Rise and Fall of the Great Powers. The book is about the centrality of economic power in international relations.

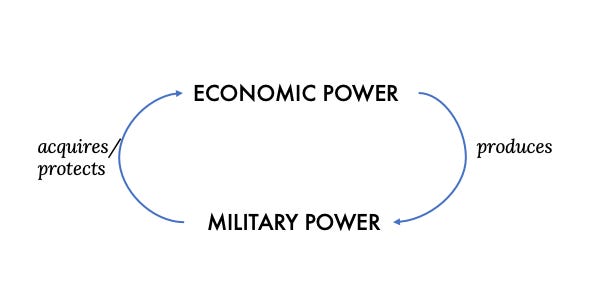

TL;DR visualisation:

In the author’s own words:

It sounds crudely mercantilistic to express it this way, but wealth is usually needed to underpin military power, and military power is usually needed to acquire and protect wealth. If, however, too large a proportion of the state’s resources is diverted from wealth creation and allocated instead to military purposes, then that is likely to lead to a weakening of national power over the longer term. In the same way, if a state overextends itself strategically - by, say, the conquest of extensive territories or the waging of costly wars — it runs the risk that the potential benefits from external expansion may be outweighed by the great expense of it all..

The reason I’m interested in this book now is that the guns vs butter debate has made a comeback. The argument goes that India has no choice but to contain its defence expenditure now in order to make fiscal space for spending on public health and education.

This to me is a false dichotomy. We do need to cut government expenditures but not in a way that reduces military firepower. To explain why I say so, look at this simple model below.

The solid line represents the government of India’s budget constraint. The argument that we need to trade-off military firepower for expenditure on meritorious services such as health and education assumes that we are at point B already i.e. these two goods already account for most of the government expenditure.

However, the reality is that we are somewhere at point A i.e. total government expenditure on health/education and military firepower both, is way below the budget constraint.

All government spending combined is nearly 26 per cent of India’s GDP. Of which ~2.1 per cent of GDP is allocated towards the Ministry of Defence, ~1.4 per cent of GDP is public health expenditure, and ~4.6 per cent of GDP is the total expenditure on education. That’s a total of 8.1% of GDP. It’s the remaining ~18 per cent of GDP that needs more scrutiny.

Where does this remaining amount go, you ask? Apart from expenses on social welfare, some of it in the form of explicit and implicit subsidies, and some more on government’s expenditure on itself. Read this by TN Ninan in ThePrint:

pension liabilities grew rapidly because of greater longevity, inflation-adjustment, and generous Pay Commission hand-outs, not to mention the one-rank-one-pension decision by the Narendra Modi government in its early days, fulfilling an election promise and sending defence pensions soaring. For the army, as a result, the pension bill has overtaken the pay bill. For the railways, the bill for pay and pensions (including productivity-linked bonuses for an organisation with static revenue) has risen to two-thirds of all costs. For the defence forces, it has climbed to nearly 60 per cent, even as the government is forced to freeze weapon purchases for lack of money.

In short, India’s case does not yet require a sharp trade-off between government expenditure on defence and health/education. In fact, we need to increase both. There’s enough slack elsewhere. The COVID-19 crisis is a good opportunity to reconsider some of these irrational expenses.

Lights, Camera, (Policy Precedes) Action: The Unresolved Question of Naya Daur

Public Policy via Bollywood

— Raghu Sanjaylal Jaitley

Naya Daur (A New Era, B.R. Chopra, 1957) made during the high noon of Nehruvian socialism is often considered the defining cultural watermark of those times. Far from it. Naya Daur is, in fact, a stinging riposte to the Nehruvian state. It asks a fundamental question that had split even the Constituent Assembly – who should be the primary agent of change to modernise India? The state, the society, or the market? In siding with the society, Naya Daur seeks a rethink on the role of the state intervening in the lives of its people.

That the newly independent India needed to change wasn’t ever in doubt. The colonial rule had drained it economically. Its society was riven with ancient caste prejudices and practices. The enlightenment values of liberty, freedom and equality that philosophically underpinned the western democracies were difficult to root in the Indian intellectual or social context. Democracy, with equal rights to all citizens, was, therefore, an audacious gamble. But we chose that radical end.

All that remained was what means should we adopt to change India?

The market was quickly dumped as an option. The imperialist plunder that was seen as the handiwork of markets, the influence of Fabian socialism and the apparent miracle of central planning in the Soviet Union were enough to silence the pro-market voices. One would have assumed that the Gandhian vision centred on the society would have seen the market — that emphasises the merits of voluntary exchange between individuals — in more favourable terms. But that was not to be either.

The society and the state, therefore, were the two poles around which the debates coalesced. This was the classic Burke versus Paine debate on new territory. The proponents of the state included trenchant critics of the Indian society like Nehru and Ambedkar. Deeply suspicious of the Indian society, they wanted the state to remain consciously detached from it while working to change it from outside. Gandhi, Mukherjee and Kriplani placed the society as the most acceptable agent of change and wanted the change to emerge from within. Gandhi believed strong moral suasion and the efforts of the volunteers of the (disbanded) Congress who would fan out to the lakhs of villages would bring about true swaraj in India. The power of the state would devolve down to a village collective who would use that judiciously (not coercively) within its unique context to bring swaraj for all.

The statists won. Our constitution was to be more than a legal construct. It was to be a tool for social revolution engineered by the state. And, so began a schism in the Indian polity. The state was run by liberal-minded modernists who viewed the customs and traditions of the Indian society as impediments to progress. The common citizenry, on the other hand, viewed the rootless elite presiding over the state as a substitute of the colonial power who would ‘rule’ over them with, possibly, greater benevolence.

Rousseau in The Social Contract (a book that launched a thousand revolutions) describes an ideal society where “the peasants are among the happiest people in the world regulating the affairs of state under an oak tree.” “The simple and upright peasants" were happy because the "general will" of the entire community was being expressed and was so "manifestly evident that only common sense is needed to discern it." The village of Naya Daur is the Rousseaun ideal. There are hardworking men and women who are deeply connected to their land with a benign feudal overlord who was part of the social fabric. There isn’t a wisp of the casteist and superstitious cesspool that Ambedkar or Nehru so wanted to upend.

Naya Daur is a masterly crafted plot with multiple strands running through the movie – a love triangle, a friendship gone sour, man versus machine and the village as the locus of change in society. It begins with this quote from Gandhi. You know where the film’s sympathies lie.

The lives of Dilip Kumar (tangawallah) and Ajit (woodcutter) and their hardworking friends change when Jeevan, the son of the village zamindar, returns after his education in the city. Jeevan represents both the market and the instincts of the Nehruvian state that want to change the village from the outside. He automates the sawmill first that hits the livelihoods of the woodcutters. Things come to a head when Jeevan decides to introduce a bus service to the famous temple nearby. This route is what earns the tangawallhas their daily daal-roti. Dilip Kumar objects and a bet is placed. There will be a race between the tanga and the bus to the temple; whoever wins gets their way. Meanwhile, Dilip Kumar and Ajit, vying for Vyjanthimala’s affections, fall out with some ‘hand of God’ support from Chand Usmani. Ajit joins the dark side with Jeevan while Dilip Kumar and the villagers begin building a bridge that will cut short the distance to the temple for the tanga and give it a fighting chance against the bus. The usual last act drama ensues with man winning the race against machine. Dilip Kumar sums it up at the end when he claims the villagers aren’t against machines but want them in their lives on their terms. Let the society decide how it wants to change.

The cast, with an outstanding performance by Dilip Kumar, is first-rate. The film established O.P. Nayyar as a top-notch composer and the script (Akhtar Mirza, father of Saeed) and the direction move the film along briskly tying up the multiple sub-plots to perfection at the end.

The point that remains unresolved is why did Chopra name the film Naya Daur? Did man winning over machine herald a new era? Or, was the title a touch satirical? That the new era won’t arrive through a state-led intervention until you co-opt the society into the modernisation project. The role of the state has remained a principal axis of divergence in the Indian political discourse. These questions have greater salience today as the society questions the shibboleths on which the constitution and the modern India project was built. That favourite question of Amit Varma in his superb podcast The Seen and The Unseen – whether a liberal constitution was imposed on an illiberal society – is timely as the democratic mandate seems to offer legitimacy to the efforts of diluting the constitution.

Naya Daur was a huge commercial success. Not merely because the underdog won. Rather, it showed a mirror to the foundation of Indian society. The reflection we saw confirmed our biases. We weren’t as bad as the state made us out to be. Naya Daur has a message for the liberals who wring their hands in despair about the path India is going down today.

The society isn’t the problem. Within it, possibly, lies the solution.

India Policy Watch: Frozen 3.0

Insights on burning policy issues in India

— Raghu Sanjaylal Jaitley

The corporate bond market is freezing up. RBI is exhausting all its indirect options of boosting liquidity gradually. There’s a clamour for more direct options. For once, not doing anything seems to be the preferred alternative by the government.

One of the abiding myths in investing – debt is safer than equity – is unravelling at this moment. For reasons that behavioural economists can explain, a debt instrument offering 12% return appears less risky to a retail investor than a similar equity instrument. But then debt funds are like Imtiaz Ali films. They all look similar, yet they are different in their own ways. You get taken in by their past reputation, they take you on a self-discovery trip and at the end, you wonder why you spent money and time on this.

The fixed-income fund managers over the years have been adding into their portfolio lower-rated paper to improve the yield to maturity (YTM – the anticipated return if the instrument is held till maturity) that they can use to attract newer investors. Some fund houses like Franklin Templeton took the considered strategy of investing in AA-rated and below paper for a lot of their debt funds with the confidence of picking winners among lower-rated papers while avoiding the banana skins. Corporate treasuries looking for that extra return and retail investors thinking debt is safer subscribed to these funds. Now, this is all fine if the following conditions are met:

The credit risk environment is stable or getting better. This means the economy is doing well, companies are putting up a strong showing and improving their credit ratings.

The bond market is liquid and has depth. So, when you have to sell a block, you find buyers at various price points.

The corporate governance practices are robust, and you get adequate early warning signals about any risks from their disclosures.

The credit rating agencies discriminate adequately so the credit risk differential reflected in their ratings of two papers is in sync with the actual spread between them

It isn’t too difficult to see from the above what’s happened to the bond market in India over the last two years. The economy has slowed down and companies in various sectors have struggled. The bond market that has always been shallow has fewer good quality and liquid options. Further, we have been hit by a series of surprises like the AAA-rated IL&FS defaulting and large corporates like Jindal Steel, Essel, Vodafone and DHFL running out of funds and luck. Lastly, the rating agencies haven’t discerned the true risk differential between AAA and sub-AAA ratings. Rating agencies have often followed than led in forecasting trends.

And, then we got the COVID-19 lockdown which has led to a cash flow crisis for most organisations. Corporates weren’t able to repay or rollover their debts. The corporate treasuries looking for cash started redeeming their investments. The funds quickly used up the cash they keep aside for redemptions. They could borrow up to 20 per cent of their assets under management from banks. They used this limit up as well. They then started selling their holdings. This was possibly the worst time to find buyers. They sold their highest quality bonds first and took losses to offload them to meet their obligations. But the redemption pressure by now turned into a ‘run’ on these funds. Informed investors wanted to get out as quickly as possible. Also, as the fund house sold the papers that were ‘saleable’, they were left with less liquid and worse assets. This meant the remaining investors would take a greater hit. The fund house had no other option than to freeze these funds.

This, in summary, is what happened to the six funds of Franklin Templeton.

The industry body AMFI and a whole host of industry voices have come out assuring investors this is a one-off event of a fund house playing the high-stake game of investing in lower-rated papers. A lot is being made about how they represent only 1.4% of the total industry AUM. But here are the imponderables:

There’s NBFC stress that’s building up. NBFC customers have been offered the three-month payment moratorium but NBFCs themselves haven’t been given the relief for their borrowings from banks. So, a lot of NBFCs aren’t getting any money from their customers but they have to repay. The NBFCs can’t default on their bond maturity payments else future borrowings will be under risk. The estimates might vary but it is safe to assume about Rs. 1.5 Lakh Crores of redemption is coming up by June. If a lot of them default, debt MFs will have to take a haircut.

RBI has offered targeted long-term repo operations (TLTRO) to pump liquidity and have banks buy corporate bonds. But as the undersubscription of TLTRO 2.0 has shown, banks aren’t keen on picking up any kind of risky paper in these times. Smaller NBFCs have an existential threat looming over them.

The impact of COVID-19 on different sectors and companies is still unclear. How many of the AAA-rated companies will be able to make a quick recovery or will still retain a business model that isn’t affected in a post-Covid scenario is unclear? Also, the redemption pressure on debt funds could continue as corporates struggle with cash flow issues. The shallow bond market will struggle to support this.

There are three possible policy responses to this. One is for RBI to step in and buy bonds directly to boost liquidity. RBI acts as a buyer of the last resort. This will eliminate transmission loss and contain any fallout of a large number of NBFCs failing. Second is for the TARP-like programme that seems to be favoured among analysts sitting outside India. Both these options involve government funding and taking risks on its books. The last option is to let RBI run its gamut of options including another TLTRO and stand aside doing nothing thereafter. There will be a shakeout among the NBFCs and their defaults will lead to a cascading impact across the financial system. Banks and MFs will take a hit. But that’s capitalism; too bad if you get hurt. How many bailouts can the government do?

If you can’t survive a 3-month stress test, you weren’t meant for the long run.

HomeWork

Reading and listening recommendations on public policy matters

[Blog post] V Anantha Nageswaran wonders what’s stopping the government from coming up with a bold fiscal support plan. He refers to the idea of a separate COVID-19 budget to ringfence expenditures, which is quite interesting.

[Article] I have an article in the Deccan Herald on the ingredients required to convert a crisis into a policy opportunity.

[Podcast] We were on The Seen and the Unseen discussing the means and ends of Indian foreign policy.

[Book] The Logic of Collective Action. Mancur Olson’s classic on the politics and economics of concentrated benefits versus diffused costs.

That’s all for the week. If you like this newsletter, please do share.

If you like the kinds of things this newsletter talks about, consider taking up the Takshashila Institution’s Graduate Certificate in Public Policy (GCPP) course. It’s fully online and meant for working professionals and has three specialisations: Technology Policy, Public Policy, and Defence & Foreign Affairs. Applications for the May 2020 cohort are now open. For more details, check here.