#342 Quick-fire

Decoding Hungarian Election Results, India's Dog in the US-China Fight on AI chips, and Five Crucial Developments in Tech Geopolitics

Global Policy Watch: Hungary Kya?

Global issues and their impact on India

—RSJ

It’s good to be back after a two-week break. Much has moved in the interim, but the underlying picture remains familiar. West Asia sits in a tense ceasefire, with the U.S. and Iran settling into a holding pattern that neither side seems inclined to disturb. The former is relying on the slow grind of economic pressure, while the latter works around it through land routes, informal channels, and partial flows that keep the system from tightening fully.

For countries like India, much of Southeast Asia, and parts of Europe, the effects are beginning to register in ways that are more immediate than strategic, as oil prices firm up and supply becomes less predictable, setting the stage for second-order effects. If this persists into May without resolution, shortages will begin to move from the abstract to the tangible. By then, the domestic political calendar will have shifted as well, with election results behind the government and us in a position to act through price pass-through, tighter distribution, or some form of rationing in the more sensitive segments of the economy.

The inflationary impulse from such a shock rarely stays contained within fuel; instead, it moves through transport, packaging, and any sector where petroleum derivatives sit within the cost structure. Add the risk of an El Niño year and the possibility of a weaker monsoon, things tighten further, as fertiliser prices continue to rise globally, and urea shortage risks look real for the Rabi season (we have enough for Kharif sowing). There is bound to be fiscal policy action by the end of this quarter.

High-frequency indicators for April suggest some moderation in the economy, though nothing sharp enough to force a reassessment. The next few weeks will begin to shape the policy response, and once the election cycle clears, both fiscal and monetary choices and actions will offer a clearer signal of how seriously these risks are being taken. We will have a lot to chew on in the future editions on this.

For this edition, let me start with a minor gloating point.

At the beginning of the year, I had made my usual set of predictions (edition #329), one of which was this:

“Surprisingly, in 2026, Europe will buck the trend of right-wing parties gaining ground in elections. I think the overt support from the MAGA crowd plus the US national security strategy document published last month that openly seeks to support “patriotic European parties” and “to help Europe correct its current trajectory” will backfire. The firm stand by the current leaders to Trump’s bullying, to China’s dumping and promised manufacturing stimulus will steal some of the thunder of the right. The result of this will be seen in their underperformance across the board: of Farage’s Reform UK in the midyear local elections, AfD losing what seems like a slam dunk now in state elections in Germany and similar setbacks in France and the Netherlands for right-wing parties. And, in perhaps the most visible sign of this, Orban will lose in Hungary this April.”

Yeah, I had called it at the start of the year.

Of course, like all such forecasts, this is just good fortune. A fluke. But I hadn’t provided one vital piece of information in that post.

The basis for that call was not a model or a decisive piece of information, but a sense that something in the prevailing narrative did not quite hold, shaped in part by the week I spent in Budapest last year. Over the following months, I returned to Hungary in fragments, reading more closely and tracking developments while trying to reconcile the dominant story of political stability with the less tangible signals I had observed both while I was there and in my conversations with people. I planned on writing about Hungary more than once over the last year, only to leave the piece unfinished each time because something else, more pressing, came up.

Now that the result is known, it is tempting to impose clarity on what were in reality scattered impressions. But I thought it was best to finish that long-pending post on Hungary in this edition. We are all wiser after the event, of course. But in my defence, I had made this prediction four months back.

In January, when I made the prediction, there wasn’t much in the public domain to support that view. Most commentary assumed continuity. Orbán had been in power long enough to have reshaped institutions, aligned the media, and built a durable political base. I didn’t have a specific trigger for my prediction. A week is not enough to understand a country, but it is enough to notice when things don’t quite line up.

Budapest itself presents well. The central parts are efficient and in line with what you would expect from a European capital. Move out of that zone, and the picture changes. Infrastructure weakens, maintenance slips, and in the countryside, the general state of disrepair becomes clearer.

Alongside this was a second layer of economic ambiguity. Hungary had drawn in European manufacturing investment about a decade back, and it was also seeing increasing Chinese interest, which was working to undercut the EU by setting up a base there. On paper, that diversification looks sensible. But the idea that Orban could take EU funds, use its membership as a lever to draw in investments from Europe and then become the first port of call for China to set up their assault on European manufacturers seemed too precious. I could sense the EU tap would run dry soon. And it did.

Politically, the surface looked stable. Orbán’s version of nationalism had not lost support in any obvious way. Positions on immigration, culture, religion, and family still had broad acceptance. There was no strong ideological pushback in everyday conversations. If anything, those ideas had become part of the baseline. That is where the shift had begun. After more than a decade of dominance, the ideology had done its work. It had defined boundaries and built a narrative. There are only so many times you can return to the same themes before they stop adding energy. At some point, the question changes from whether people agree to whether the ideology is still doing anything for them.

That change was visible in how discussions moved from identity to utility. People were not arguing against nationalism; they were asking what it was delivering at this stage. Hungary’s relationship with the European Union, the steady friction with it, and the position taken on the war in Ukraine had started to feel less like a clear strategy and more like a set of positions without an obvious payoff. The proximity to Vladimir Putin added to that. EU funds had been an important part of the economy, and questions around their use and future availability were part of the conversation. None of this led to open opposition, but it introduced doubt.

There was another strand that came up in a few conversations, which helped make sense of the broader picture. Some people described Hungary under Orbán as a kind of model for the global right, a place that had shown how to build what he had called an “illiberal democracy.” The comparison that came to mind for them was Fidel Castro, not in terms of ideology but in terms of role. A country that becomes a reference point, a leader who stands for something larger than his own electorate. A system that sees itself as a model begins to behave like one. It leans into its narrative and becomes less flexible. That works when a system is set up in opposition to the outside world. It is harder when it is embedded within it. Hungary is part of the European economic and political structures. It cannot operate as a permanent outlier without incurring costs. The more the narrative moved in that direction, the more the gap between posture and reality widened.

That gap became more visible as Orbán’s international profile grew. Alignment with figures like Donald Trump and attention from right-wing movements across Europe increased his standing outside Hungary. Inside the country, it created a different reaction. Nationalism is built on the idea of sovereignty and independence. It does not sit comfortably with visible external influence, even when that influence comes from ideological allies. When politicians from other countries begin to engage with domestic politics, it raises questions. The idea that nationalist movements across countries would operate in alignment carries its own contradiction. It suggests coordination that runs against the premise of autonomy. What can a global group of bigots rally together for? Demonising the global Left? Yes, perhaps. But beyond that, if all right-wing, populist movements want to make their nations great again, how will any bilateral discussions among them be a mutual win-win?

All of this played out in an environment where public debate was limited. The media was co-opted, dissent was not visible, and there was little space for open disagreement. In private conversations, there was more questioning than the public discourse suggested. That is the setting in which what is described as a preference cascade can take shape. People hold back their views because they assume they are in the minority. The absence of visible dissent reinforces that assumption. When someone credible breaks that pattern, opinions that were already present begin to surface quickly.

The emergence of Péter Magyar needs to be seen in that context. He did not build a campaign on ideological opposition to Orbán. He stayed within a similar broad frame on nationalism and conservative positions and shifted the focus to governance, corruption, and the sense that the system had become self-serving. That mattered. It meant that voters did not have to change their beliefs to consider an alternative. They only had to reconsider who was best placed to act on those beliefs. Magyar did not create dissatisfaction; he made it visible and usable in a political sense.

Over the months after that visit, I kept coming back to these threads to see if they held. Economic divergence remained. The strategic ambiguity in foreign policy continued. The nationalist narrative did not change in substance. The gap between global positioning and domestic concerns widened. None of these on their own was decisive. Taken together, they pointed to a system that was no longer adjusting. It was maintaining itself, but without resolving the tensions within it. Systems can run like that for a while. They tend not to do so indefinitely.

Hungary is not a template that can be applied elsewhere without adjustment. It is smaller, more tightly connected, and shifts in sentiment can move through it faster. It is also a case where the challenge to the incumbent came from within the same ideological space rather than from a clear opposite. That is a specific configuration. In larger countries, with more complex social and political structures, similar outcomes are harder to produce.

What that week in Hungary provided me was a set of inconsistencies that did not resolve over time. Political outcomes often look sudden when they arrive, but the conditions for them build gradually. If you pay attention to where narratives stop aligning with lived experience, you can see that build-up before it shows up in polls or results. That was the basis of the January prediction. It was about recognising that the system was no longer fully coherent on its own terms.

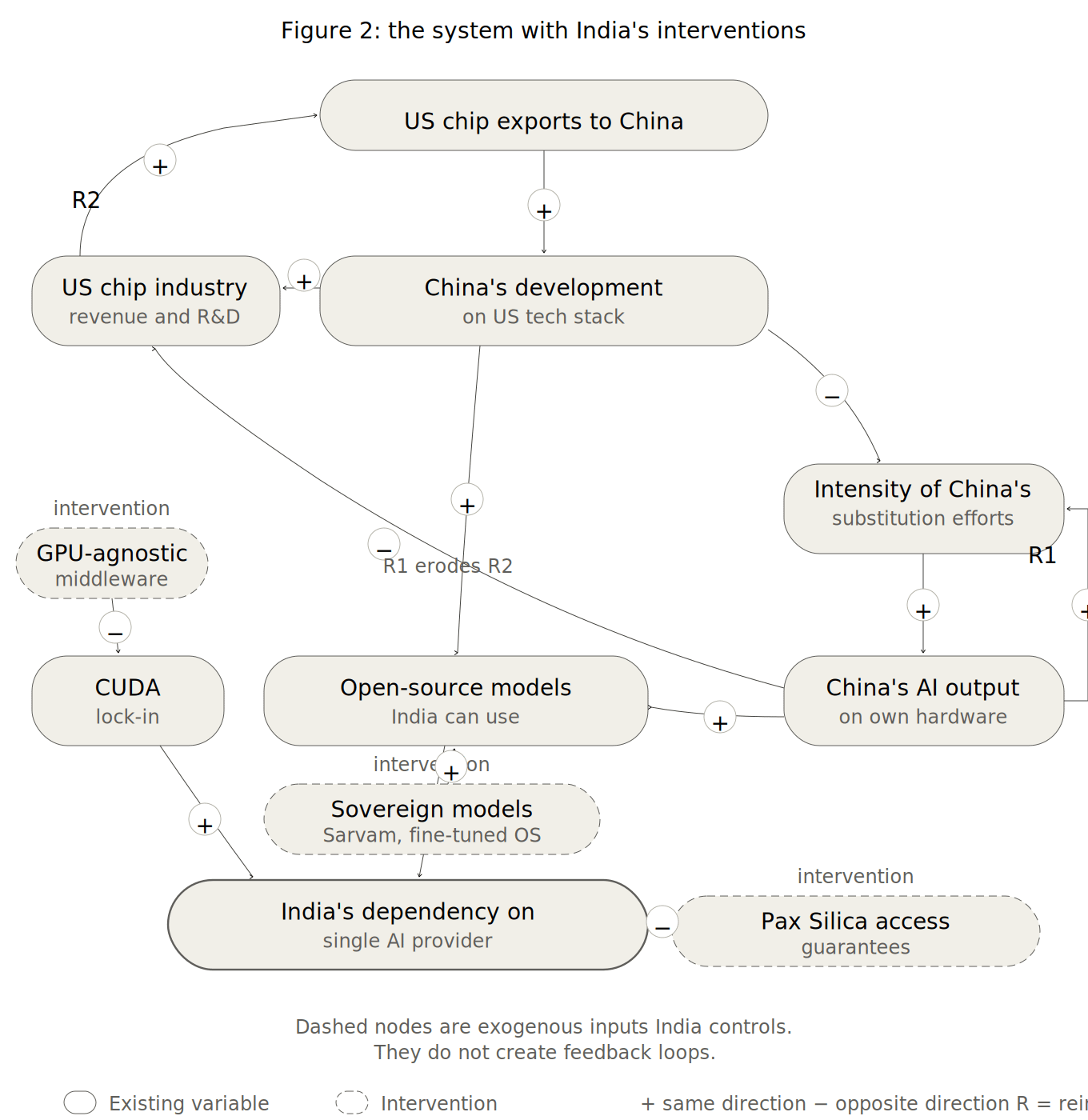

Matsyanyaaya: India Has a Stake in the US-China Fight on Advanced GPUs

Big fish eating small fish = Foreign Policy in action

—Pranay Kotasthane

Jensen Huang has long wanted to sell advanced AI chips to China. Dario Amodei, on the other hand, has compared doing so to selling nuclear weapons to North Korea and then bragging that the missile casings are made by Boeing. For most of 2025, this was a debate about American interests.

But the outcome of this debate will determine whether India has just one or many sources of advanced computing infrastructure. It will also determine whether Chinese AI labs continue to release open-source models that Indian companies use to build applications. This is not a US-China question alone.

The Biden administration’s October 2022 export controls on advanced chips to China rested on a clear causal chain: deny chips, deny compute, deny AI capability. The controls succeeded at the first link. China cannot manufacture leading-edge chips at scale; its SMIC foundry remains stuck at around 7nm, while TSMC has moved to 3nm and below. On this narrow measure, the denial worked.

But the wider chain is broken. DeepSeek, Moonshot, and Qwen emerged as frontier AI labs despite the curtailed access to chips. Huawei reported revenue of CNY 880.9 billion in 2025 and invested a record CNY 192.3 billion in R&D in the same year. Chinese AI researchers still constitute roughly half the global talent pool. The controls bought time on the manufacturing side, perhaps two to three years on leading-edge nodes. But they did not buy any meaningful time on the AI capability side, at least not in the sense that the US got to this Brahmastra first and then used it to deny others access to it.

Jensen Huang made this point in the much-discussed interview with Dwarkesh Patel. As he likes to put it, AI is a five-layer stack: energy, chips, infrastructure, models, and applications. American policy sacrificed the chips layer to protect the models layer, while China adapted across the other four layers with abundant energy, algorithmic innovation, and a large engineering workforce. The chips layer matters, but it is not the only layer that matters.

India’s position in this five-layer stack is distinct from both the US and China. At the applications layer, India has the right ingredients. Its IT services sector could become the global delivery platform for enterprise AI deployment. At the chip design layer, every major fabless semiconductor company, including those driving the current Nvidia debate, runs large Global Capability Centres in India. Indian engineers are central to the chip architectures being contested.

But below those two layers, India is dependent. India’s data centre capacity is an order of magnitude smaller than that of the US or China. Energy constraints limit the ability to compensate for chip quality with raw compute volume. India imports advanced chips and, despite Sarvam AI’s 105B-parameter multilingual model in March 2026, will continue to import frontier models too.

This consumer-integrator position creates a strategic calculus that neither Jensen Huang nor Dario Amodei represents. India does not want China to dominate all five layers of AI infrastructure. India also won’t prefer to use China’s AI chips. But India also does not benefit from a world in which access to advanced chips is contingent on the policy preferences of the US administration, which reversed its own H20 policy four times in three years. India definitely benefits from China’s open-source AI ecosystem. DeepSeek and Qwen are not threats to Indian AI ambitions; they are inputs. Indian companies use these open-source models to build products and services. The more competitive the global model ecosystem, the less leverage any single country holds over India’s access to frontier AI capability.

Open-source models are separable from Chinese hardware. Indian firms can optimise Qwen’s weights without deploying Huawei Ascend chips. The security concern India legitimately has is about hardware, not about models. A Chinese chip with undisclosed firmware in critical infrastructure is a genuine risk. An open-source model that has been fine-tuned is not as big a threat.

India should therefore want Chinese AI labs to keep releasing open-source models. It should want that ecosystem to remain competitive with American proprietary models. It should not want Huawei hardware anywhere near sensitive Indian infrastructure. The current American debate collapses this distinction, treating Chinese chips and Chinese models as the same threat. For India, they are not.

India has three tasks at hand. Through its engagement in Pax Silica, the US-led technology initiative that India joined in early 2026, it has an opportunity to articulate a specific position rather than defer to Washington’s framing. Second, funding for GPU-agnostic middleware is vital. Public investment in open alternatives to reduce the CUDA lock-in should become a priority for the India AI Mission. Third, India should maintain model pluralism as a deliberate strategy. Use American proprietary models where they are best. Use Chinese open-source models where they are useful. Build sovereign models like Sarvam for applications where dependency on foreign providers is unacceptable. A pluralist global model ecosystem is structurally safer for a country in India’s position.

The causal loop analysis below captures this logic.

For more, check my paper on this topic.

Global Policy Watch: Tech Geopolitics ICYMI

Global issues and their impact on India

—Pranay Kotasthane

(This section was first posted on Technopolitik — our technology geopolitics newsletter. Subscribe to it here.)

1. NDRC, not SAMR, blocked the Manus-Meta deal

The proposed acquisition of Manus by Meta was stopped by China’s National Development and Reform Commission (NDRC), not by the State Administration for Market Regulation (SAMR). This distinction is significant.

SAMR is the antitrust regulator. It blocks deals on competition grounds. China is known to use this instrument for national security reasons, but it often does so under the guise of anti-monopoly or consumer harm. You’ll find more about SAMR’s actions in this post.

NDRC, by contrast, is the macroeconomic planning body. Its intervention signals that China views this deal not as a competition problem but as a security problem. If NDRC is now the effective gatekeeper for tech mergers & acquisitions, that suggests Chinese AI firms are no longer commercial assets subject to normal market rules. They are national assets, and their disposition is a matter for economic planners, not antitrust lawyers.

Meanwhile, the NDRC had banned two co-founders of Manus from travelling abroad since March this year, citing this regulatory review. Tough times for a Chinese technology firm—foreign companies see you surreptitiously, and even if you manage to convince them, the CPC blocks the sale. This is exactly the problem that rare-earth refiners in China have been facing due to stringent controls over the past 12 months.

2. The wrong lessons from Mythos

The Anthropic Mythos model, whose cyber-offensive capabilities led Anthropic to delay its public release while American companies patched their software, has become the centrepiece of the case for chip export controls. The argument, most prominently made in the Dwarkesh-Huang exchange, runs like this: if China had more compute, it could have trained Mythos first. And that would be unacceptable to the US and the world because of the harm it would cause.

This framing has three problems.

The first is the frame itself. Mythos-type capabilities do not structurally change national power the way nuclear weapons did. Thinking of AI through the nuclear lens, where getting there first and then denying others is the only viable strategy, leads to bad policy. For countries like India, AI is better understood as a vital, general-purpose technology: something you want widely available, not concentrated in one place.

The second problem is the assumption of asymmetry. The argument treats Chinese offensive cyber use as a given while treating American use as defensive. Both countries have offensive cyber capabilities, and both have used them. The real problem is not Chinese malice in particular; it is the absence of credible governance mechanisms for AI deployment, a problem neither Washington nor Beijing has solved.

The third problem is the most important for India. The Mythos episode shows that if AI models can find thousands of unpatched vulnerabilities in major software systems, then every country running those systems is exposed, including India, regardless of who trained the model. The lesson is about defensive readiness and software hygiene, not about chip exports.

3. What made Taiwan think ITRI’s spinoffs should be private?

Karthik Tadepalli has a lovely essay on ITRI, the Industrial Technology Research Institute that seeded Taiwan’s semiconductor industry, in the Asterisk magazine. He finds that ITRI demonstrates how a focused, applied R&D institute can build a world-class chip industry by starting small, training people, and serving firms rather than competing with them.

One question worth thinking over: what led Taiwan’s planners to assume that ITRI’s spin-offs should be private firms? The default in most developing countries, and certainly in India, was the opposite. C-DOT had genuinely good technology, including telephone switches that were competitive by any standard. BEL had developed strategic IP. But neither institution could imagine letting go of the downstream functions. They did engage private players, but merely as “vendors” rather than partners. The IP stayed inside the public sector and did not compound.

Taiwan’s answer to this question is the crucial variable in the ITRI story. It was not just industrial policy; it was industrial policy with a particular theory of ownership and incentives. Getting that theory right is what allowed TSMC to become TSMC rather than a government procurement vehicle.

4. Heavy rare earths outside China, for the first time in two decades

Lynas has begun heavy rare earth production at its refinery in Malaysia, reports the Wall Street Journal. Apparently, this is the first time in twenty years that a heavy rare earth refinement on a commercial scale has happened outside China.

This is a direct consequence of Chinese coercion. Beijing’s export restrictions on rare earth processing, imposed as leverage in the broader technology dispute with the US, accelerated the diversification it was meant to deter. China+1 is happening, not because of Western industrial policy alone, but because China’s own actions have raised the cost of dependence.

The Lynas development will not resolve the structural imbalance overnight. China still dominates processing capacity. But the direction of travel is now clear, and it is being driven as much by China’s behaviour as by any Western strategy.

5. Tech companies as military targets

My colleague Nitin Pai makes an uncomfortable argument in a recent essay that tech companies, which have become entangled in military operations, are now legitimate targets under international humanitarian law.

The legal standard is whether an entity makes “an effective contribution to military action.” Palantir’s AI targeting tools, Microsoft’s communications infrastructure for US-Israeli operations, and the sanctions imposed on Russia at Washington’s behest are not incidental. Palantir CEO Alex Karp has said explicitly that tech firms owe the US government their support, given the historical conditions that allowed them to grow. That is a coherent position, but it has consequences. You cannot claim both the returns of geopolitical alignment and the protections of civilian status.

The Indian implication is that the more India’s critical systems depend on foreign tech infrastructure whose owners have chosen sides, the more India’s infrastructure is exposed to the targeting logic of conflicts it has no role in. This is not a hypothetical. It is the architecture of the current moment. Nitin’s conclusion is to reduce dependence on foreign tech for critical systems and increase defence spending to protect what cannot be reduced.

HomeWork

[Puliyabaazi] Since geopolitics is the flavour of the decade, we got the brilliant Atul Mishra to decipher international relations from first principles.

[Puliyabaazi] We had another terrific masterclass by MR Madhavan on what exactly transpired in the Parliament in the special session a couple of weeks back.

[Audio] Check out this wonderful little Radio Netherlands audio piece from 1994 on what had changed in India since the economic liberalisation. The title (Microchips yes, Potato chips no) refers to a quote by Murli Manohar Joshi that encapsulates Indian policymakers’ confused approach to imports.

[Repo] Turn a non-fiction epub or PDF into a 35–45 minute podcast episode and publish it to a private RSS feed you can subscribe to from any podcast app.

In the context of the geopolitics post, it (weaponization of the economy) is not a recent phenomenon. The weaponization of the economy began after 9/11, as explained in Henry Farrell and Abraham Newman's book, Underground Empire: How America Weaponized the World Economy.

It didn't start with that intention, of course. Rather it started with the intent of tracking terrorist money movement across borders post 9/11. Gradually, America realized it could weaponize the global financial system for other reasons too. When Europe and China didn't seem too keen to isolate Iran (Obama era), the US realized any tech having at least x% of American IP could also be weaponized. The reasons and means for weaponization of the economy have only been steadily increasing over the last 2 decades. The book is an interesting read.

The R1/R2 framing is useful for thinking about India's position. Though if the R1 loop is sustained for a few years, it might lead to less separability between models and hardware. As Ascend matures and training of models is increasingly optimised for Ascend, the separability might decrease. Chinese open-weight models might still be portable but practically optimised for Ascend. India could still run them on Nvidia chips but at a worse cost-per-token than achievable on Ascend. The weights are still available, but the cost advantage that makes them attractive erodes.

If that's right, R2 has a second-order benefit. Not just access reliability, but continued CUDA compatibility of the Chinese open-weight ecosystem because Chinese labs keep training on Nvidia hardware. Under R1, India still gets open-weights, but they drift away from India's infrastructure over time.

Perhaps this is not a real concern; cross-compatibility incentives (Chinese labs wanting global deployment) might still keep the stacks convergent.